Cooperative Banks in India hold a unique place in the country’s financial landscape due to their conception and working. Offering a community-focused approach to banking, they are crucial for facilitating financial inclusion, particularly in rural and agricultural sectors. This article of NEXT IAS aims to study Cooperative Banks in detail, including their meaning, types, structure, significance, and more.

Cooperative Banks refer to those financial institutions under the Banking System in India that operate on the principles of cooperation and mutual benefit for their members.

| – They are incorporated and registered under the States’ Cooperative Societies Act passed by the concerned state. – The National Bank for Agriculture and Rural Development (NABARD) is the apex body of the cooperative sector in India. |

These banks in India, broadly, come under the dual control of:

| Basis of Difference | Commercial Banks | Cooperatives Banks |

|---|---|---|

| Formed as | Joint-stock Banks. | Co-operative organizations. |

| Governing Act | Banking Regulation Act 1949. | Co-operative Societies Act of 1904. |

| Regulation | Subject to the control of the Reserve Bank of India directly. | Subject to the rules laid down by the Registrar of Co-operative Societies. |

| SLR and CRR Requirements | Relatively Higher. | Relatively Lower. |

| Services Offered | Larger scope in offering a variety of banking services. | Lesser scope in offering a variety of banking services. |

| Area of Operation | Large-scale operation, usually countrywide. | Small-scale operation, usually limited to a region. |

| Main functions | Mostly provide short-term finance to industry, trade, and commerce, including priority sectors like exports, etc. | Usually cater to the credit needs of agriculturists. |

| Rate of interest | Offer lower rates of interest on deposits compared to co-op banks. | Offer a slightly higher rate of interest on deposits. |

| Borrowers | Borrowers of commercial banks are only account holders and have no voting power as such, so they cannot have any influence on the lending policy of these banks. | Borrowers are member shareholders, so they have some influence on the lending policy of the banks, on account of their voting power. |

| Flexibility in lending | Commercial banks are free from any rigidities in terms of lending options. | Co-operative banks do have not much scope for flexibility on account of the rigidities of the bylaws of the Co-operative Societies. |

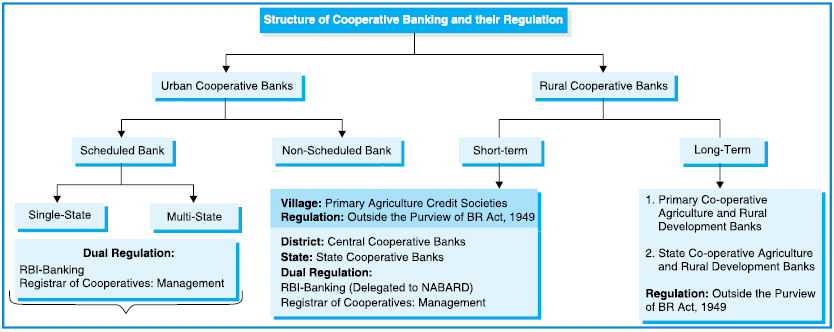

These banks, under the Banking System in India, are primarily categorized into – Rural Cooperative Banks (RCBS), and Urban Cooperative Banks (UCBS). They are further sub-categorised as shown below:

State Cooperative Agriculture and Rural Development Banks (SCARDBs) focus on providing long-term credit for agricultural and rural development purposes.

Primary Cooperative Agricultural and Rural Development Banks (PCARDBs) are aimed at providing financial services to rural areas, especially to small and marginal farmers, agricultural laborers, and rural artisans.

Due to their very nature of working, they play crucial roles in the Indian economy. Some of their major roles can be seen as follows:

By enabling easy access to institutional credit to under-banked sections, Cooperative Banks in India are pivotal in the socio-economic development of the country. Their role remains crucial in the promotion of small industries, self-employment, and businesses that may not meet the stringent requirements of larger banks. With the changing economic and technological landscapes of the country, these banks have the potential to empower more rural and urban communities, driving forward India’s agenda of inclusive growth and economic development.

In light of the crises related to some UCBs, the Banking Regulation Act, 1949 was amended through the Banking Regulation (Amendment) Act, 2020. It is aimed to bring all the UCBs and Multi-State Cooperative Banks under the direct supervision of the Reserve Bank of India (RBI).

The first Cooperative Bank in India was the Anyonya Co-operative Bank (ACBL), established in 1889 in Vadodara, Gujarat. It is no longer operational now.

They come under the dual control of the Reserve Bank of India and the Registrar of Cooperative Societies of the respective state or central government. While the RBI regulates the banking aspects, the Registrar of Co-operative Societies regulates management-related aspects of these banks.